Buying a House in Australia

Buying a house in Australia is an exciting milestone and, for many migrants, an important step towards building long-term security and a sense of home. Australia has a well-regulated, transparent property market, and while the process is generally straightforward, there are some additional rules and considerations for non-citizens and temporary residents.

Most property purchases involve several key steps, including securing finance, finding the right property, making an offer, and completing legal and construction checks before settlement. Properties are commonly sold through private sale or auction, and once a contract is signed, it becomes legally binding.

If you are not an Australian citizen or permanent resident, you may need approval from the Foreign Investment Review Board (FIRB) before purchasing residential property. In general, temporary residents are permitted to buy established homes to live in, while foreign investors are usually restricted to new properties. These rules are designed to help manage housing supply and availability.

It’s also important to budget for additional costs beyond the purchase price. These can include stamp duty (a government tax that varies by state), legal or conveyancing fees, building and pest inspections, and loan-related expenses. Some buyers may be eligible for government incentives, such as grants or stamp duty concessions, particularly first-home buyers.

The legal transfer of ownership is handled by a licensed conveyancer or solicitor, who ensures all checks are completed and funds are transferred correctly at settlement.

While the process may feel unfamiliar at first, with the right guidance and preparation, buying a home in Australia can be a smooth and rewarding experience—and an important step in creating your new life here.

Buying and selling can be VERY quick compared to the UK. When you sign your purchase contract, you will know the completion date. There are reasons why this date may not be met but it is clear and delays will be agreed upon during the transaction if any become necessary.

Australian buy / sell transactions do not generally get into a ‘chain’ situation, each sale or purchase stands alone as its own transaction.

FIRB Rules Explained Simply

If you are not an Australian citizen or permanent resident, you may need approval from the Foreign Investment Review Board (FIRB) before buying property.

In general:

Temporary residents (such as temporary visa holders)

You can usually buy:

- One established home to live in

- New homes

- Vacant land (if you build within a set timeframe)

These rules exist to help manage housing supply.

Foreign buyers may also pay:

- Additional stamp duty surcharge

- Additional land tax

Always get professional advice before buying.

Click on the picture on the right to go to the FIRB website to find out more

Step-by-Step Process: Buying a House in Australia (Not auction)

Step 1: Finance Pre-Approval

Before looking at houses, speak to:

- A bank, or

- Mortgage broker

They will tell you:

- How much you can borrow

- Your budget

This is called pre-approval.

Step 2: Start Looking at Properties

You can:

- Attend open homes

- Contact agents

- View properties online

When you find a suitable property, you can request:

Strata report (for apartments)

Contract of sale

Best websites to use are:

In Australia, properties for sale are commonly shown through scheduled “open homes,” where the property is open to any interested buyers for a short set time (often 15–30 minutes on a Saturday), allowing multiple people to walk through at once without an appointment. This is quite different from the United Kingdom, where viewings are usually private, one-on-one appointments arranged through the agent. At an Australian open home, it’s important to be prepared and observant: agents may ask you to sign in, and they will often watch for serious buyers. You should take note of property condition (cracks, damp, smells, noise, storage, and natural light), neighbourhood factors, and how much competition there is from other buyers, as this can indicate demand. It’s also wise to ask for the contract of sale, price guide, and recent comparable sales, and remember that open homes are not just for you to assess the property — the agent is also assessing you as a potential buyer.

Step 3: Make an Offer

You can make an offer:

- Verbally, or

- In writing

You can include conditions such as:

- Subject to finance

- Subject to building and pest inspection

If accepted:

You sign the contract. This becomes legally binding.

In Australia, the usual process when buying a house is a bit different from the UK.

First, you sign the contract of sale once your offer is accepted, but the contract often has conditions built in to protect you.

The most common one is a building and pest inspection condition, which lets you check the property for structural problems, termites, or other issues. After signing the contract, you organize the inspection within the timeframe allowed (usually 7-10 days). If the inspection finds serious problems, you can negotiate repairs, ask for a price reduction, or walk away without losing your deposit. But if there’s no inspection condition, once you’ve signed, you’re generally legally committed to buy.

The other clause you would usually have in your contract would be “subject to finance”. This means that if you are then unable to secure finance you are able to end the contract. But if there is no finance clause, again, once you’ve signed, you’re generally legally committed to buy.

If you are a cash buyer, then you would not include the finance clause. If you are a builder or a home inspector, you might not include the building and pest clause.

When you offer, you usually state your preferred timescale, which is typically 30 days. This means you know when you will be moving in.

You can include any clauses you like into the offer, but they might not be accepted by the seller.

Sometimes, in a situation where there are multiple offers on a property, the seller will choose the one with the least clauses.

So although you offer, your offer may not be accepted and there may be some negotiation required to reach terms that all parties are happy with.

Often with an offer, you will sign the actual contract and put forward all your clauses. The Real Estate Agent will then take that contract to the seller, and if they sign, then your offer is now locked in and you are legally bound to purchase the property, subject to the clauses you put into your offer.

There is no chain, there is no gazumping or gazundering, there is no waiting months for anything to happen with the solicitors and all the other people in the chain. This is your contract on this property and you now know exactly what you need to do by when or face financial (or other) consequences for breach of contract.

Once your offer is accepted and your contract drawn up, you will generally pay a deposit at this point, of 5-10% of the purchase price. This is required instantly so you will need to ensure you have this available. You can negotiate a lower deposit but this will need to be done in your offer.

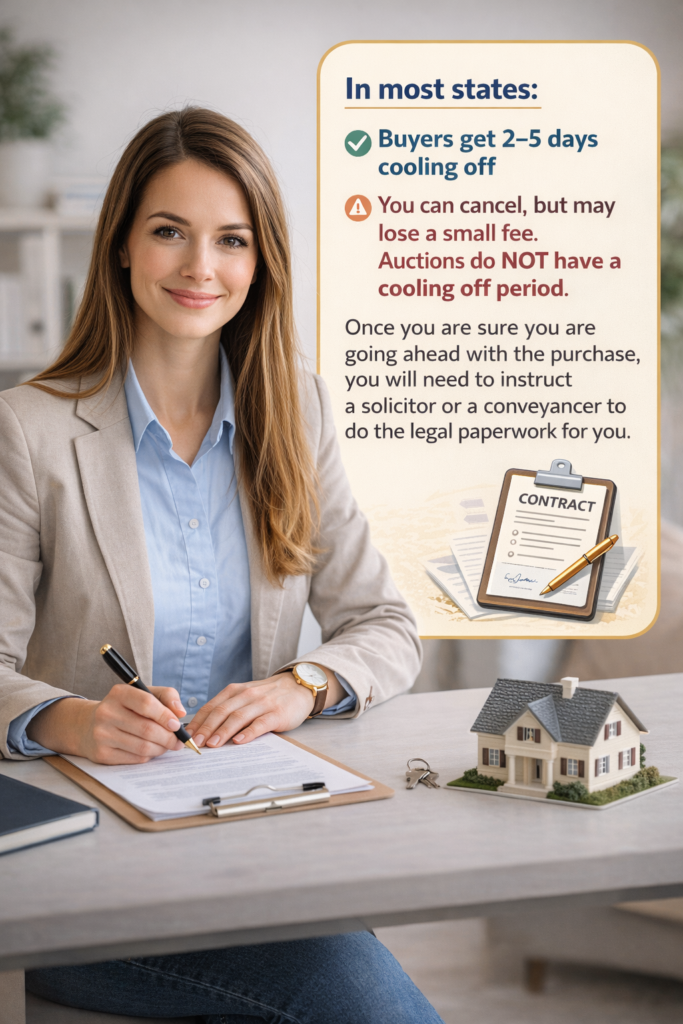

Step 4: Cooling Off Period (Not Always Available)

In most states:

- Buyers get 2–5 days cooling off

You can cancel, but may lose a small fee. Auctions do NOT have a cooling off period.

Once you are sure you are going ahead with the purchase, you will need to instruct a solicitor or a conveyancer to do the legal paperwork for you.

Step 5: Meet Your Clauses

Have your Building and Pest Inspection done within the allowed timeframe. This inspection checks:

- Structural damage

- Termites

- Safety issues

This is very important because property is generally sold “buyer beware”, meaning the contract does not guarantee building condition. In the UK, there are different ‘pests’ and building issues. In Australia, termites are a big problem in some areas, and building insurance will not pay for any damage that they cause.

If major problems are found, you may:

- Cancel contract (if conditions allow) or

- Renegotiate price to account for any defects found.

At the same time, you will also need to be organising your finance – if this is one of your clauses. Your broker will help you to do this if you are using one, otherwise you need to move forward with your pre approval with whichever financial institution offered this to you. You will need to stay on top of these items to ensure that you meet the deadlines set out in your contract.

Australian banks and other lending institutions, as well as the building and pest inspectors are used to this quick turnaround.

Step 6: Going Unconditional

Once your obligations have been met, you are happy with your building and pest report and you have your mortgage offer if you need one, your legal representative will advise you that you are ready to go unconditional.

This is the point of absolutely no return.

Once you go unconditional you can then book your removalists as the house will be yours on the date agreed.

Step 7: Preparing for Settlement (completion)

Settlement usually takes:

- 30 to 90 days – but you will know the exact timeline as it will be in your contract

During this time:

- Your lender prepares the loan and

- Legal transfer paperwork is arranged

- Your legal representative will ask you to send them the money you are putting in, as well as other monies owed to them for stamp duty, their fees and anything else that has been agreed – maybe you are buying something else from the seller in the home.

- You arrange contracts with utilities suppliers for your new home.

- You arrange removalists if you need them

Step 8: Settlement Day

This is when:

- Your legal representative pays the seller using your funds and the mortgage funds

- Ownership transfers to you

- You receive your keys.

Settlement is usually booked in for a certain time, so you will know that your settlement is occurring at say 3pm and shortly after that you should receive a phone call advising you that settlement DID occur and the house is now yours.

You now own the home. Congratulations!!

Buying a Home at Auction

Auctions are a popular method for selling homes in Australia, especially in major cities like Sydney and Melbourne, with around one in five properties typically sold this way in busy markets. A property is “passed in” when it doesn’t reach the seller’s reserve price during the auction. Even if a property is passed in, interested bidders can still negotiate with the seller after the auction to try to secure the home.

In the UK, houses are often sold at auction if there is something wrong with them or the title. In Australia, this is usually not the case. It is a way of generating a sale for the best price and a guaranteed deal if it sells on auction day. Although you need to do your research, it is just a different way to sell a normal property.

- The auctioneer/agent cannot tell you the reserve price (the minimum the seller is willing to accept) before the auction — this is confidential.

- They can tell you if the property is “passed in” after the auction if the bidding doesn’t meet the reserve.

- Agents may provide price guidance from previous sales or market appraisals, but they cannot guarantee the reserve or tell you the exact amount.

- It’s common for agents to suggest a guide or expected range, but it’s still up to the bidder to make their decision.

- The reserve price protects the seller and disclosing it would undermine the auction process.

Bidders should do their own research, inspect the property, and have finance ready, rather than relying on the agent for exact pricing.

Buying a property at auction is different from a private sale because once the auctioneer’s hammer falls, the sale becomes unconditional. This means the buyer is legally committed to purchase the property immediately, with no cooling-off period and no ability to back out if finance isn’t approved. Because of this, it’s crucial to organise your finances, obtain pre-approval for a mortgage, and have a building and pest inspection completed before the auction. Auctions can be competitive, but they offer a transparent, fast, and definite way to secure a property, and the process often helps establish the market value through open bidding.

If you go to an auction and wish to bid, you will need to register. To do this you will need to take some identification with you. The agent can normally advise you what they need in this respect before the day of auction.

Typical Costs of Purchasing a Home in Australia

| Cost | Approximate Amount |

| Deposit | 5%–10% |

| Stamp duty | 3%–7% |

| Legal fees | $800–$2,500 |

| Building inspection | $400–$800 |

| Pest inspection | $200–$500 |

| Loan fees | varies |

| Moving costs | varies |

Stamp duty is usually the biggest cost after the house.

Stamp duty is a government tax paid when buying property, and the amount depends on property value and location.

Stamp Duty in Each Australian State

Stamp duty rules vary by state. This is the situation as at February 2026 but please check that these are still correct. Click on the state title to go to the state website for stamp duty (or transfer duty)

These sites do have a calculator too so you can work out your own stamp duty. It can be high, so make sure you can pay it as it is due on completion (settlement)

| State | How it works | Typical Rate | First Home Buyer Stamp Duty Help |

| New South Wales | Progressive scale | Up to 5.5% | Exemption up to $800k |

| Victoria | Progressive scale | Up to 6.5% | Exemption up to $600k |

| Queensland | Progressive scale | Up to 5.75% | Exemption up to $700k new homes |

| Western Australia | Progressive scale | Up to 5.15% | Exemption up to $450k |

| South Australia | Progressive scale | Up to 5.5% | Full exemption for new homes |

| Tasmania | Progressive scale | Up to 4.5% | Exemption up to $750k |

| Australian Capital Territory | Progressive scale | Up to 6.4% | Multiple concessions |

| Northern Territory | Formula system | Up to 5.95% | Concessions available |

Stamp duty uses a sliding scale, meaning higher property values pay higher tax rates.

Foreign buyers may also pay an extra surcharge.

First Home Owner Grants (FHOG) in Each Australian State

In Australia, first home buyer grants are designed to help people purchasing their first home reduce the upfront costs of buying property. These schemes vary by state and territory, but they generally include stamp duty (transfer duty) exemptions or reductions (see above), and in some cases, cash grants for eligible buyers, particularly for new or newly built homes. The aim is to make it easier for first-time buyers to enter the property market by lowering the financial barriers, while also encouraging the construction of new housing. Eligibility rules usually include being a permanent resident or citizen, buying or building your first home in Australia, and meeting property value thresholds, so it’s important to check the specific requirements for your state or territory before applying.

If you have owned a property anywhere in the world, you are generally not considered a first time home owner.

This is the current information as at February 2026

| State / Territory | What’s Available (Grants / Concessions) | Official Link |

|---|---|---|

| New South Wales | $10,000 First Home Owner Grant for buying/building a new home (first‑time buyers). Combined with stamp duty exemptions/concessions through the First Home Buyers Assistance Scheme (e.g., no duty up to certain price caps). | https://www.revenue.nsw.gov.au/grants-schemes/first-home-owner-new-homes-grant |

| Victoria | $10,000 First Home Owner Grant available to eligible buyers for new homes up to a property value cap; plus stamp duty exemption or concession up to certain thresholds. | https://www.sro.vic.gov.au/buying-property/first-home-owner-grant |

| Queensland | First Home Owner Grant (up to around $30,000 for new builds under certain value caps). First home buyers also receive stamp duty concessions (no duty up to a threshold on established homes and concessions above). | https://qro.qld.gov.au/property-concessions-grants/first-home-grant |

| Western Australia | $10,000 First Home Owner Grant for eligible buyers of new homes; stamp duty exemptions and concessions up to specified property value thresholds (first home owner rate of duty). | https://www.wa.gov.au/organisation/department-of-treasury-and-finance/first-home-owner-grant-fhog |

| South Australia | Up to $15,000 First Home Owner Grant for eligible new home buyers; stamp duty exemptions (particularly on new builds and vacant land) depending on eligibility. | https://www.revenuesa.sa.gov.au/first-home-owners-grant (site includes FHOG details & forms) |

| Tasmania | First Home Owner Grant and duty relief available — eligibility typically includes a grant for new homes and exemptions/concessions for established homes up to a value cap. | https://www.sro.tas.gov.au/first-home-owner |

| Northern Territory | First Home Owner Grant (up to $50,000 for new homes until 30 Sept 2026 and sometimes $10,000 on established homes depending on contract date); plus various duty concessions. | https://nt.gov.au/property/home-owner-assistance/first-home-owners/first-home-owner-grant |

| Australian Capital Territory | The traditional FHOG was discontinued in 2019; first home buyers now access the Home Buyer Concession Scheme (primarily stamp duty relief). | https://www.revenue.act.gov.au/home-buyer-assistance/home-buyer-concession-scheme (for duty relief) |

The Help To Buy Scheme

The Australian Government Help to Buy Scheme is a new shared‑equity home‑ownership assistance program that launched on 5 December 2025. It’s designed to help eligible people buy a home sooner by allowing the government to contribute up to 40 % of the cost of a new home (30 % for existing homes), so you can buy with a much lower deposit (as little as 2 %) and borrow less overall.

Citizenship/Residency Eligibility

To qualify for the Help to Buy scheme, one of the requirements is that applicants must be Australian citizens who are at least 18 years old.

That means:

- New migrants on temporary visas (e.g., student visas, work visas) are generally not eligible for Help to Buy until they become Australian citizens.

- Permanent residents who are not yet citizens also do not qualify under the current rules for Help to Buy — the citizenship requirement is explicit in official eligibility criteria.

Other Requirements

Applicants must also earn under certain income limits ($100,000 for individuals, $160,000 for joint applicants/single parents as at Feb 2026)

And you must be planning to live in the home as your principal residence

For more information, click the picture to go to their site.

Land Tax

Land tax is a state-based tax in Australia that applies to the total value of land you own, excluding your principal place of residence in most states. It is calculated annually and typically affects individuals or businesses that own investment or commercial properties. Each state and territory sets its own thresholds, rates, and exemptions, so the amount payable can vary depending on where the land is located and its total taxable value. Land tax is generally used by governments to generate revenue for public services and infrastructure.

This is worth reading up on if you intend to invest in property other than your own home as it can be a surprise you didn’t bargain for! It may also be relevant if you use a trust to purchase your home.

Summary

Buying property in Australia involves several important steps, including arranging finance, finding a property, making an offer, signing a contract, and completing settlement.

Buyers must also budget for additional costs such as stamp duty, legal fees, and inspections.

Stamp duty is a government tax that varies by state and property value, and first-home buyers may qualify for concessions.

Migrants may need FIRB approval depending on their visa status.

With proper planning and professional advice, buying a home in Australia can be a straightforward and rewarding process.